What's the deal? The Tech M&A & Fundraising Newsletter - Human Capital and FinOps 2026

Human Capital and FinOps 2026

Hiring and headcount has long been a proxy for confidence. Teams scaled ahead of revenue, burn was course-corrected along the way, and runway was something to extend - not defend. That logical progression is being challenged. Fundraising cycles are longer, capital is more selective, and investors are rewarding capital efficiency over hypergrowth. The rise of AI only accelerated that trend by reshaping productivity expectations - whether these gains have fully materialised or not yet.

Welcome to What’s the Deal? - your monthly deep dive into the strategic currents shaping the tech investment landscape.

This February edition explores how human capital and AI is influencing FinOps, and what CEOs & CFOs can explore differently to protect runway, negotiating power and valuation resilience in 2026.

A note from the Editor - Claire Trachet

"Markets move in cycles, and so does the logic founders use to run their companies. For much of the past decade, hiring functioned as a measurement for growth - teams expanded in preparation for revenue rising, valuations seemingly followed. The risk of not growing headcount felt bigger than the risk of not closing the next round. Runway was something to be extended by raising more, and the mere mention of "optimising" carried an uncomfortable undertone - as if the mindset had shifted away from growth and toward fear. That logic has now evolved.

The post-2021 hangover brought a sharp correction to that era. And before it fully settled, a new cycle arrived - shaped not by abundant capital, but by the emergence of AI. The result is a moment of unusual complexity: the old rules no longer hold, and the new ones are still being written.

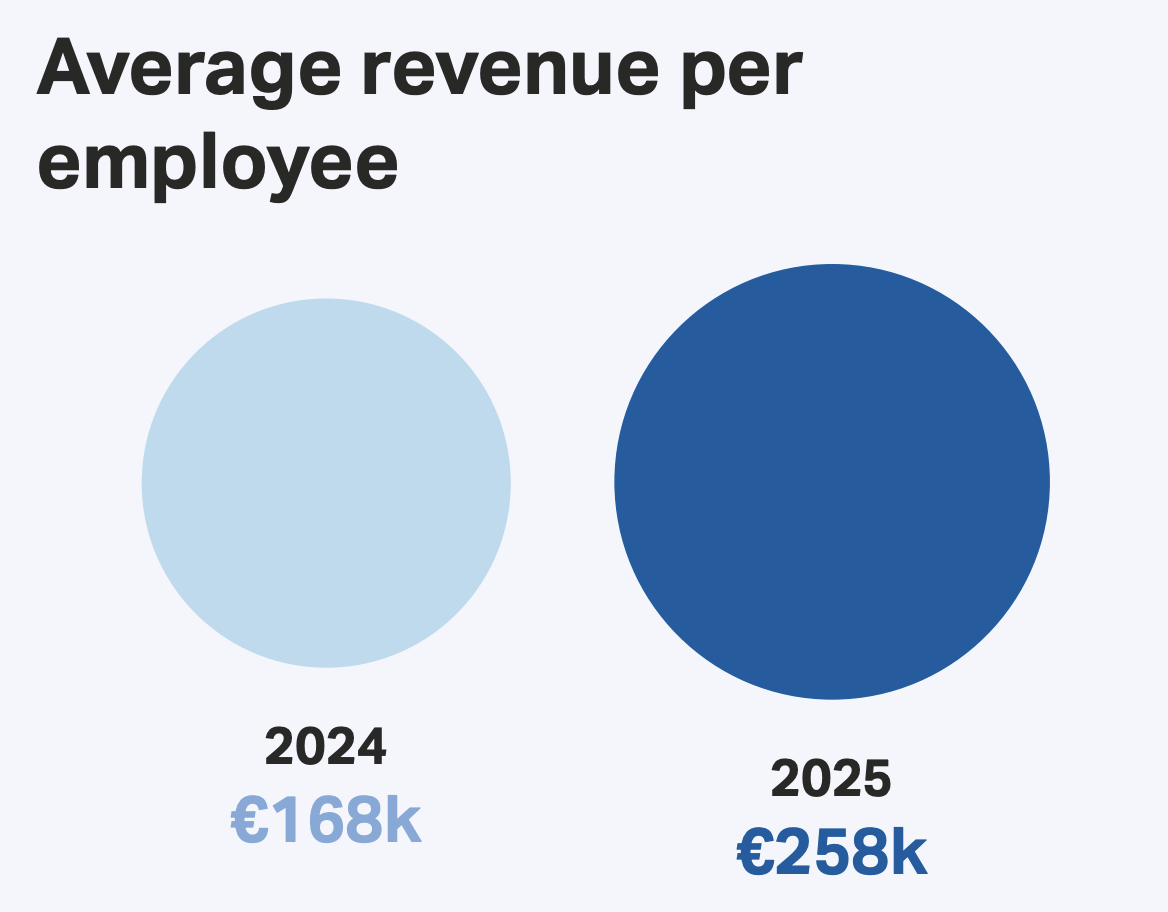

Source: Sifted 250 "Leaderboards" 2025

Among Europe’s fastest-growing startups, the latest Sifted 250 data shows average headcount edging down from 102 to 98, even as Average Revenue Per Employee (ARPE) climbed from €168,000 to €258,000 - an increase of roughly 54%. Funding per company rose at the same time, for the select few who could raise. And while this shift in the Sifted250 ARPE is due to changes in the companies industries and stage, ie not to be taken as an industry-wide benchmark, it does show a clear direction of travel: the fastest growers focus on output per head, not headcount per se.

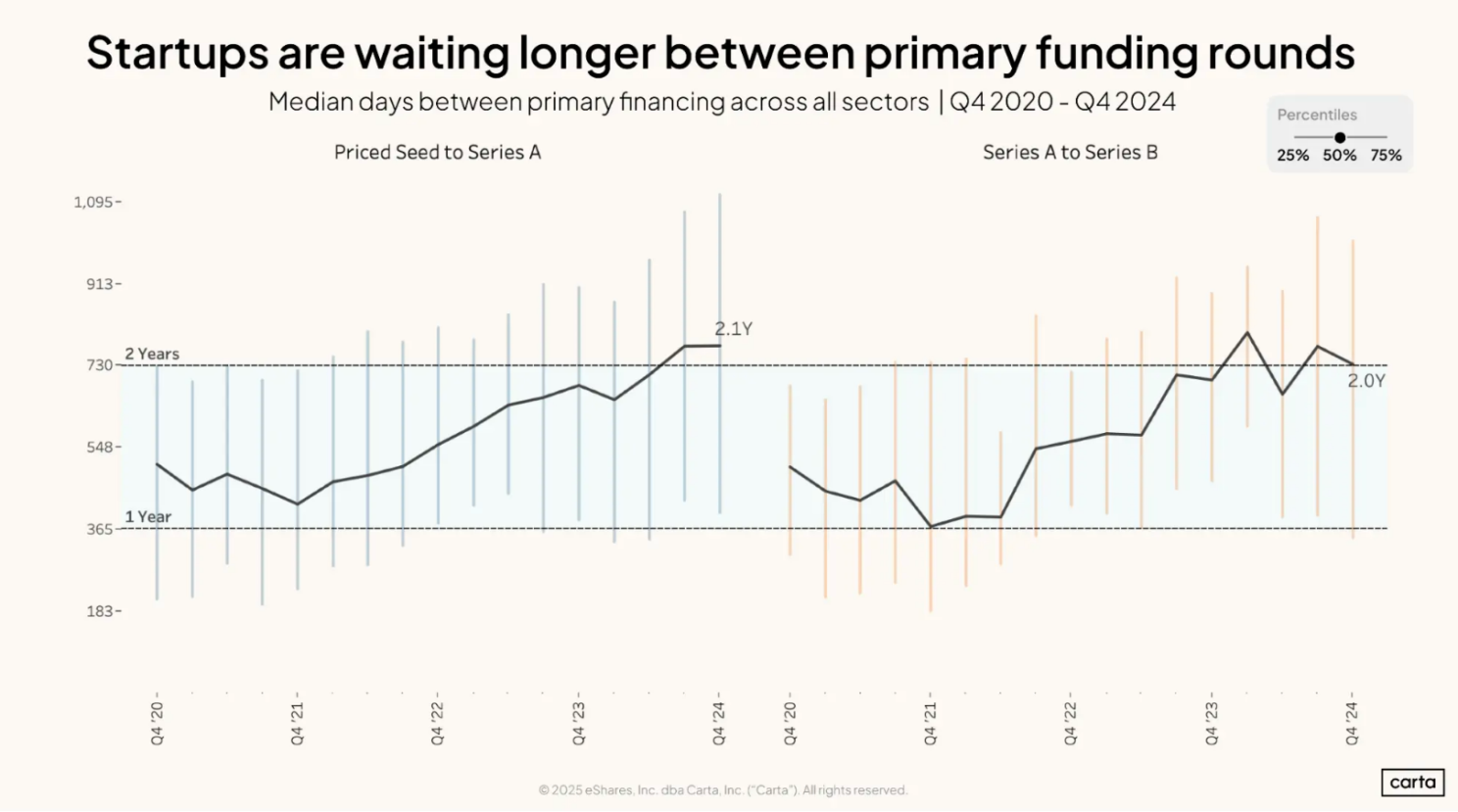

Current fundraising dynamics reinforce the point. The median time between Series A and Series B has stretched to 2.8 years - the longest on record. Nearly half of Seed deals are now bridge rounds. Down rounds, while no longer spiking, remain a meaningful share of venture financings. Capital is still available. But it is more selective and slower - essentially, the market is less forgiving of an operational learning curve as the tech ecosystem continues to mature.

Towards 2021, the time between raises was shortening to nearly 1 year - however this has incrementally increased since the valuation crash of 2021.

Source: Carta

Labour markets tell a complementary story. In the UK, vacancies have fallen below 700,000, the lowest level since the pandemic, while youth unemployment has risen and employer National Insurance contributions have increased the fully loaded cost of each hire. In the US, private hiring has also cooled and roughly 127,000 technology roles were cut last year alone. According to Challenger data, more than 50,000 announced job reductions cited artificial intelligence as a contributing factor.

This is not a collapse in employment. It is a recalibration of productivity expectations.

For venture-backed companies, that recalibration has immediate financial implications. Personnel costs are typically the largest operating expense at startups & scale-ups. Hiring decisions therefore have the biggest impact on the burn; burn determines runway; and runway, in turn, shapes how much control you have over your destiny.

Artificial intelligence complicates matters further. Adoption is now widespread - McKinsey reports that around 88% of organisations use AI in at least one business function - yet enterprise-wide productivity gains remain uneven. In some areas, such as development teams, impact can be clearer; across broader workflows, maturity is inconsistent. Investors increasingly assume efficiency improvements are achievable. That creates a quiet tension inside the finance function: productivity may be priced in before it is fully realised.

This brings a new layer of complexity. Should growth be pursued through additional hires, or through deeper automation? Should capital be raised to scale teams, or to extend runway? When does rightsizing strengthen a fundraising narrative - and when does it signal weakness? How, precisely, does headcount intensity influence valuation? Like always, it depends. And that has never been felt stronger than in the past 12 months.

In 2025-26, these are no longer operational side-questions. They are capital strategy.

Human capital now sits squarely inside FinOps. The companies that treat hiring as a financing decision - not a cultural reflex - preserve more optionality in a market that prizes discipline alongside ambition. There is no blanket answer: the right move depends on role, timing, runway and the strength of your growth engine. But the standard has changed. Build the case like you would any capital deployment: define the ROI, test it against downside scenarios, and iterate relentlessly as the data comes in - not through dramatic swings, but through consistent, accountable adjustments.

This edition sets out a practical framework for navigating that shift."

Human Capital Inside FinOps

A CFO framework for hiring, rightsizing and keeping control over your destiny.

If hiring has become more of a financing decision, it requires a financing framework.

The past cycle rewarded following established principles: scale the team in anticipation of growth and sort out finance along the way. The current cycle is less forgiving. Capital formation is slower, bridges are common, and flat/down rounds remain part of the landscape. Capital efficiency is no longer a nice to have; it is a must that will be priced based on how you can demonstrate your track-record.

For CFOs and founders, the task is not to debate whether AI will eliminate jobs. It is to determine a strategy on how headcount decisions alter runway, leverage and valuation resilience.

Below is a practical framework.

1. Start with Runway, Not Roles

Runway is not merely survival time. It is negotiating power.

With a median 2.8-year progression between Series A and Series B, and a meaningful share of companies relying on bridge rounds, the assumption that capital will arrive “on schedule” is weaker than it was.

Before approving new hires, CEOs & CFOs should model:

Base Case runway with the revised hiring strategy

Downside runway, assuming revenue is slower than expected. This exercise enables to pre-empt the tough calls and make such decisions easier if the worst came to be. Aim to keep the same runway as Base Case, or ideally extend it by 3-6 months to get time to recover the topline.

BlueSky runway, assuming "the stars align" - you get some tailwind and top-line accelerates - aim to reach clarity on where and how you push forward. These conversations often help to iteratively push up the Base Case, as every C-level of the team is challenged on both the upside and downside, thinking creatively about resources beyond their main expectations and building rationale on their hiring strategy.

A simple guardrail is instructive:

If Downside runway cannot be maintained roughly similar to the Base Case, then the Base Case strategy has "lumpy risks" that need to be explored in greater details - ideally breaking them into smaller risks chunks that can be better mitigated back to Base Case runway (such as hiring big Seniors). And if not possible, this should be made very explicit to the Board before finalising the plans or acting on such items of the strategy.

The question is not whether the hire is useful. It is whether the risk it creates is worth the loss of leverage.

2. Track efficiency KPIs - Relentlessly

The data suggests a clear market signal: revenue per employee is rising among high performers. Investors are noticing.

Revenue per employee, headcount growth relative to revenue growth, and burn multiple now serve as indicators for discipline - not looked as absolute benchmarks, but rather trends and signals.

A practical trigger:

Anytime the topline forecast isn't meant, new headcounts budgeted should be re-assessed by the CEO & CFO and, if material, the adjustment in strategy explicitly mentioned at Board-level. Expansion should be intentional, not inertia.

3. Do Not Pre-Spend Productivity

AI adoption is widespread, but measurable productivity gains are uneven. Many firms report deploying tools without redesigning workflows - some of the larger companies are feeling the pain or broad struck adjustments of the past couple of years.

The risk for CFOs lies at both extremes:

Hiring in anticipation of productivity that tooling could unlock

Cutting in anticipation of productivity that has not yet materialised

Before expanding teams in functions plausibly affected by automation - support, finance operations, sales enablement, elements of engineering - require evidence of workflow redesign and of real-life demonstrable results.

If tooling can defer hiring by one or two quarters, the capital preserved may matter more than the capacity gained. Such tools also increase the valuation of your company in that they increase your IP (not necessarily the tool but the processes and workflows created). There is an opportunity for capitalizing on past learnings and new learnings, which takes the discipline of documenting and field-testing.

4. Rightsizing Is a Timing Decision

With over 127,000 reported tech layoffs in 2025 and tens of thousands of cuts citing AI or efficiency initiatives, cost discipline is no longer a reputational hazard.

The distinction investors draw is not between companies that cut and those that do not. It is between companies that act early and those forced to react mid-process.

Rightsizing six to nine months before a raise - with clear logic and operational redesign - strengthens the narrative of discipline. Cutting during diligence signals pressure.

If rightsizing is required, sequencing is critical. Ahead of a fundraising, proactive adjustments can reinforce capital efficiency and valuation resilience. In an M&A context, however, the calculus may differ. Buyers assess continuity, integration readiness and operational depth differently than growth investors. The same decision that improves a fundraising narrative could weaken an acquisition dynamic. This is where an advisor is critical to the process.

5. Reframe Hiring as Capital Deployment

Each hire carries a fully loaded cost: salary, tax, benefits, tooling, management bandwidth - and opportunity cost.

Personnel is typically the dominant operating expense line. Incremental hiring therefore has a direct, mechanical impact on burn multiple and runway.

So the decision should be framed like capital deployment:

Does this hire increase our company's negotiating power within 12 months?

That leverage can show up as:

accelerated revenue,

structural margin improvement,

reduced operational risk, or

clearer valuation support.

If the answer is no within 12 months, it doesn’t automatically mean “don’t hire” - but it does mean the hire belongs in the downside case. Stress-test the runway impact, make the assumptions explicit, and adjust the plan accordingly. If the return case remains unclear, the decision should be deferred or reshaped.

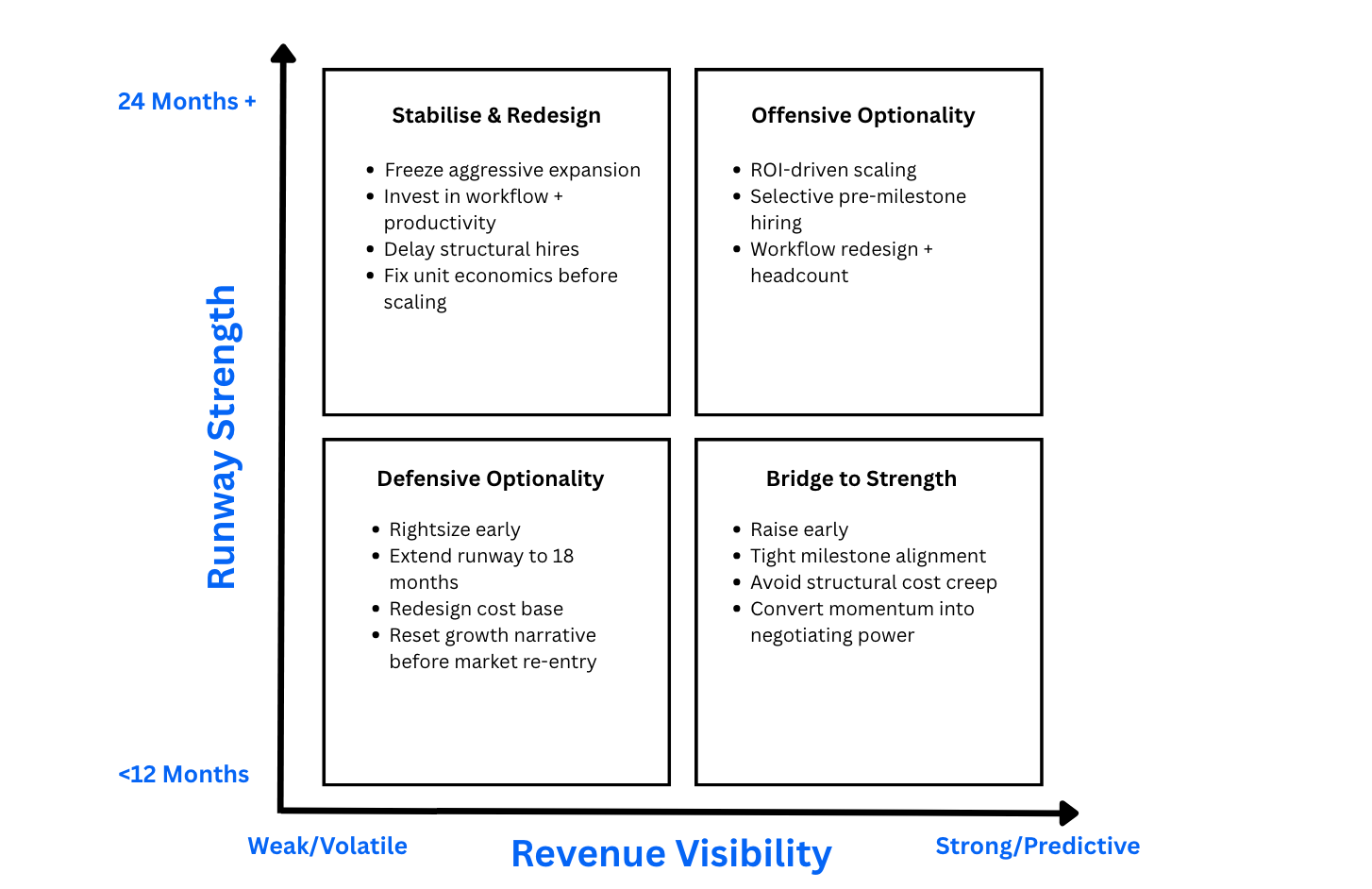

6. The Human Capital Decision Matrix for CFOs

There is no universal hiring rule in this cycle.

The right decision depends on two variables: how predictable your revenue is, and how strong your runway truly is. Revenue visibility determines how much risk you can absorb. Runway determines how much leverage you retain.

When those two move in alignment, expansion can be rational. When they diverge, risk compounds quickly - often invisibly at first.

The matrix below is not a prescription. It is a capital lens. It helps founders and CFOs position themselves honestly - and decide whether they should lean forward, stabilise, or protect.

The Human Capital Decision matrix for CFOs

The objective is not austerity. It is increasing optionality & increasing the odds.

News Roundup

Your go-to monthly roundup of Trachet in the news, key deals in the UK/EU startup arena, and emerging trends to watch.

What we’ve been reading

→ 2025 Annual Global M&A Report - PitchBook

PitchBook’s 2025 Annual Global M&A Report shows global dealmaking rebounding sharply, with approximately 50,800 deals worth nearly $5tn - the most active year on record (+12.4% YoY by volume, +37% by value). Activity was driven heavily by a surge in $1bn+ megadeals, which accounted for more than half of total deal value. The signal is not simply recovery, but concentration: larger, more complex and risk-bearing transactions are defining the cycle. With easing rates, deep private equity dry powder and AI-led growth narratives fuelling confidence in the US and Europe, 2026 looks active - but disciplined execution, valuation control and downside protection are becoming increasingly central to deal strategy.

→ SpaceX $1.25trn tie-up with xAI paves way to unite Elon Musk’s tech empire - The Times

SpaceX’s acquisition of xAI consolidates Musk’s space, satellite, AI and social media assets - including Starlink, X and Grok - into a vertically integrated technology platform reportedly valued at around $1.25tn. The strategic logic centres on control: combining data, compute, energy infrastructure and engineering talent to accelerate AI development ahead of a potential IPO later this year. The broader signal is structural. Scale players are no longer optimising for partnerships - they are collapsing ecosystems into unified balance sheets. Vertical integration, not interoperability, is emerging as the dominant power play in frontier technology.

→ Stocks Fall From Near-Record Levels Amid Tech Rout - Bloomberg

US equities pulled back from near-record highs as investors rotated away from AI-heavy megacap technology into value and cyclical names. While macro signals remain broadly supportive - easing-rate expectations, resilient growth and strong commodity pricing - sentiment around AI infrastructure spending is becoming more selective. The shift is not anti-technology; it is anti-unpriced risk. After a period of blanket enthusiasm, markets are stress-testing whether AI capital expenditure will translate into durable returns. For growth companies, valuation resilience now depends less on exposure to AI and more on proof of monetisation.

→ JPMorgan: The ‘surprising’ sector that could be ripe for M&A in Europe - Sifted

Sifted reports that secondaries activity across European tech continues to rise, providing partial liquidity to employees and early investors - but without replacing a fully functioning IPO market. At the same time, selective M&A is picking up in capital-intensive and strategically sensitive sectors such as semiconductors and quantum, driven by consolidation and sovereignty considerations. The signal for founders is nuanced: capital is available, but valuation overhangs and investor selectivity are sharpening trade-offs. Growth, partial liquidity and earlier M&A exits are increasingly active choices rather than sequential steps.

→ China’s AI surge – real threat or hype? - CNBC

The question is no longer whether China is competitive in AI - it is where that competitiveness translates into structural leverage. Chinese frontier firms such as DeepSeek are narrowing the model performance gap with U.S. leaders, even while facing export restrictions on advanced Nvidia chips. Where China differentiates is not raw compute power, but efficiency: training models with fewer chips, deploying open-weight strategies, and scaling domestic energy capacity to support AI infrastructure at speed. Combined with state subsidies and national investment vehicles, this creates a different - and potentially more cost-competitive - AI stack. The U.S., however, retains clear advantages: advanced semiconductors, frontier research institutions, hyperscale cloud infrastructure and entrenched enterprise distribution. Most analysts now expect a multi-polar AI landscape rather than a single dominant power. The competition is shifting. It is less about benchmark supremacy, and more about commercial deployment and real-world value capture.

→ Does Europe need more private credit? - Financial Times

Private credit is expanding rapidly, with global AUM estimated at $2.3tn (Preqin). Yet even within asset-backed lending - around $575bn - it remains a small slice of the $10.3tn broader asset-backed finance market across Europe and the US. The argument from Oliver Wyman is straightforward: Europe may need deeper private credit markets to fund long-duration, capital-intensive projects - particularly AI data centres and green infrastructure - where banks face regulatory constraints and public markets lack duration flexibility. The FT’s Alphaville strikes a more cautious tone, questioning whether capital supply is truly the binding constraint. In many cases, planning permissions, energy capacity and regulatory bottlenecks may be the real friction points. If a long-duration funding gap does exist, private credit could fill it - but only if investors accept illiquidity and patient capital dynamics.

We’re keen to hear about the key challenges (or opportunities!) shaping your company’s objectives in 2026. Email me at claire@trachet.co for more information on topics you'd like to see discussed in future issues of What’s the deal?