What's the deal? The Tech M&A & Fundraising Newsletter - Exit Economics

Exit Economics

Exit valuations are the ultimate measure of success for VC portfolios. Yet what sits between an exit valuation and a founder's bank balance post exit is rarely discussed as openly!

That’s what this edition is for. Our J-curve newsletter led to important conversations, which prompted the Trachet team to build the Exit Calculator - a tool designed to help founders visualise what different paths actually mean for their outcome, and to better understand the trade-offs behind each decision.

Welcome to What’s the Deal? - your monthly deep dive into the strategic forces shaping the tech investment landscape. This March edition focuses on Exit Economics - not to encourage founders to sell early, but to bring clarity to the decisions between raising, waiting, and exiting, and what each path truly means in practice.

A note from the Editor – CEO Claire Trachet

"Startup fundraising rounds travel quickly through the ecosystem. Exit outcomes rarely do.

"Before jumping in, we think it's important to make one thing clear: this edition is not an encouragement for founders to jump out early early and exit. Nor is it a case against building large, ambitious companies and a thriving European ecosystem. Quite the opposite. If Europe is to build enduring, category-defining businesses, that will require capital to flow efficiently and not stay stuck if a high growth company gets on a slower track. That's actually in the best interests of the whole ecosystem, starting with investors and founders.

"Most founders we speak to are focused on their next round. Fewer have modelled what that round actually does to their outcome. A company raises a £25 million Series B and the headline signals momentum - but it doesn't show how the T&Cs impact the proceeds of all stakeholders, especially not what the founder will actually walk away with... in different scenarios.

"Following our newsletter on the J-curve - and the volume of conversations it prompted - that question kept surfacing. Founders understood the J-curve in theory and asked about the practical implications to their specific situation: if I raise again, how do I know if/when I would actually end up better off? How much further does the outcome have to go to justify the dilution and how long does it take to get to the other side?

"Recent market data makes that question more urgent. According to PitchBook, roughly two-thirds of unicorn IPOs in 2025 priced below their last private valuation - with Klarna and Navan trading around 60% below their IPO price, Netskope around 35%, and Chime approximately 25%. Secondary markets tell a similar story, with many pandemic-era companies trading at discounts of between 33% and 61% to their last private round, according to Stifel and Forge. In Europe, roughly 98% of venture-backed exits now occur through M&A - compared to around 14% in 2021 - with IPOs remaining a limited and selective path.

"The risk isn't failure. It's staying stuck - raising another round to extend the runway without materially changing the trajectory. The J-curve works when the outcome on the other side justifies the dilution and the time. When it doesn't, founders lose years and ownership, while investors lose the capital efficiency they were underwriting... or simply returning capital faster to their LPs! In the vast majority of cases, nobody wins from a delay of "doing more of the same" if financed with VC money. That's just not the purpose, and alternatives exist, from other financing strategies to exit.

"What founders often don’t realise is that investors are already running that calculation. Within 12 to 18 months of an investment, most investors have a clear view of which bucket a company is heading toward. For companies not on a path to a top-tier outcome, returning capital sooner can be a rational portfolio decision - and while it might not be obvious, it often also is a better alternative for founders.

That is where clarity matters.

Trachet's Exit Calculatorwas built to support getting to that clarity, through discussions. It is a simplified tool designed to translate headline valuations into real outcomes - showing how ownership, dilution, and exit value interact across different paths. It is not a recommendation to sell or to raise, but a way to prompt better questions, support more informed discussions, and give founders a clearer view of their options - including in conversations with investors.

Because, in most cases, founders hold ordinary shares and so they share the destiny of the "least favored" shareholders of the CapTable. If a decision thus makes sense for founders, it tends to be the best outcome for the other stakeholders too... unless the CapTable is "broken"! Bur that's for another newsletter!

Some companies should absolutely continue raising and building. Others may find that an exit or strategic process creates a better outcome than another round. The point is not to push one path over another. The point is to bring hard data into decisions that are too often shaped by momentum, emotion, or misaligned incentives.

There is no single right answer. But there is value in seeing the full picture.”

Trachet's Exit Calculator

This simplified tool has been built to support discussions and decision-making. With 8 key assumptions to input, it allows founders to compare outcomes between an exit today and an exit following a subsequent funding round - and to understand not just the potential proceeds, but the opportunity cost attached to each path.

It is designed for speed and directional clarity. For more complex situations or tailored analysis, we encourage you to get in touch.

Below, we map out two scenarios to illustrate how these dynamics play out in practice. The two scenarios below look at similar cybersecurity SaaS businesses at different stages - one at Series A, the other at Series B - facing the same core question: what is the best trade-off between a certain outcome now and taking on dilution, time, and execution risk for a potentially higher - but less certain - exit. How much would an additional round need to add to the valuation and would the company still be in potential buyers' sweetspot at that level?

Together, these scenarios illustrate how stage, timing, and opportunity cost shape the decision - and why the same question can lead to very different answers.

Scenario 1:

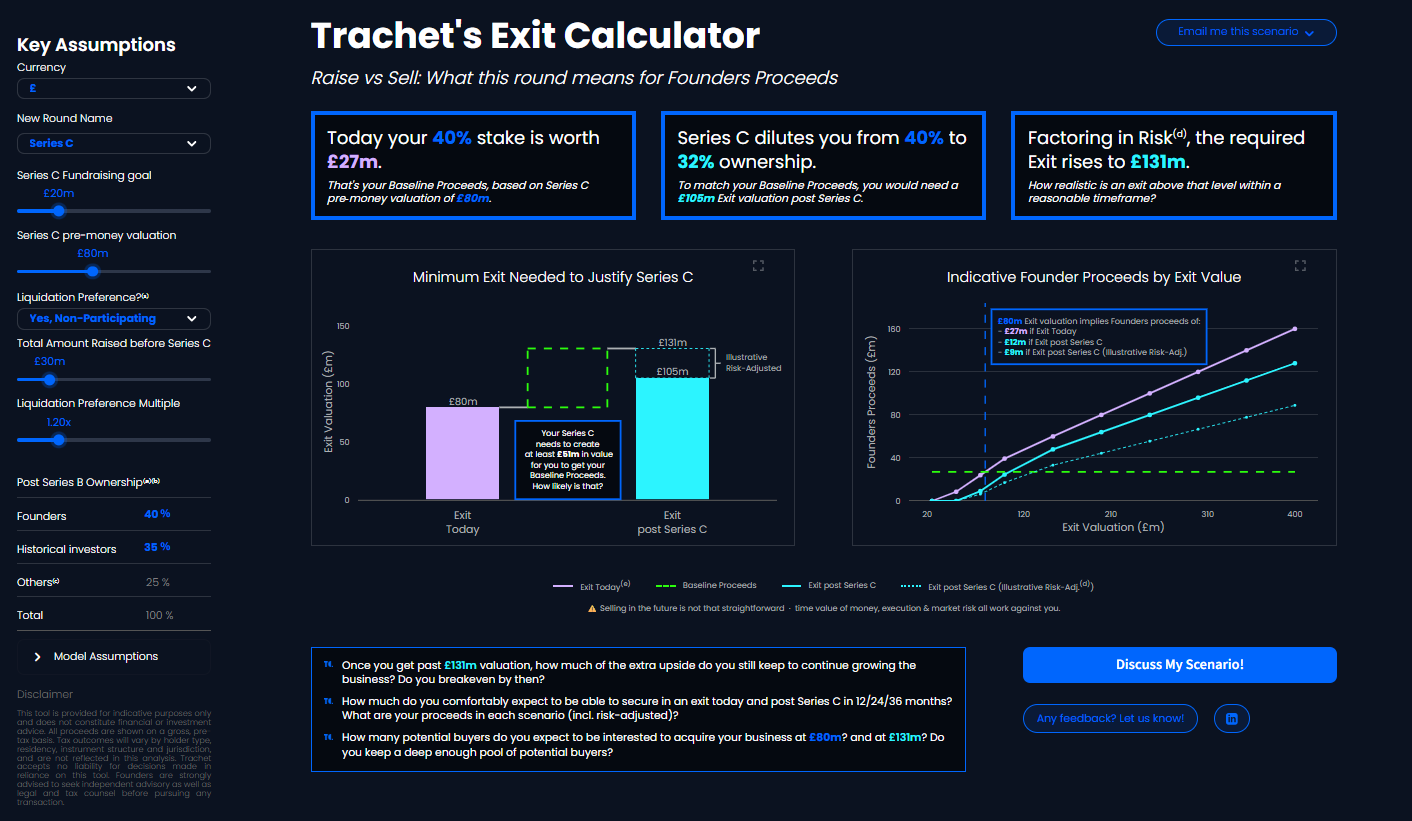

Company X is a London cybersecurity SaaS company post Series B

Company X is contemplating a Series C after raising £30m to date. A strategic buyer is prepared to pay around £80m today - the product fits neatly into their existing enterprise stack, the cross-sell opportunity is obvious, and the synergy value is real now rather than theoretical. Revenue numbers continue growing, however below 50% YoY as sales remain vastly driven by the initial core product. Revenues in new geographies is also not strong enough yet to move the needle on valuation.

In the calculator, that translates into a clear starting point. With founders owning 40%, their stake is worth £27m today under the "Exit Today" scenario (ie based on the Series C pre-money valuation of £80m). If Company X raises a £20m Series C instead, ownership falls from 40% to 32% - meaning the business needs to reach £105m under the "Exit post Series C" scenario just for the founder to stand still versus the "Exit Today" Baseline Proceeds, before risk is even considered.

That may not sound impossible on paper, but it is where the story matters. The roadmap for the next 12–24 months don't point to any obvious step up in buyers appetite. The core product is understood, the most natural acquirer is already at the table, and the next phase is execution: more sales capacity, more rollout, more delivery. Useful, but unlikely to be transformational.

The "Exit post Series C" path only makes sense if there is a credible buyer universe above £100m - with enough depth to generate real competitive tension in a future process. If the majority of potential acquirers cluster below £100m acquisitions value, the argument for waiting weakens considerably and relies on potential PE funds having appetite for this type of business at a higher revenue level... but the multiple might be lower than the current situation.

Once execution risk is reflected in the calculator, the picture sharpens further. The "Baseline Proceeds" on a risk-adjusted basis require roughly a £131m exit just to match what is available today - in other words, Company X would be taking dilution and time risk in the hope of achieving a meaningfully higher outcome than the one already on the table.

This is the classic case where an exit is likely preferable: a strategic premium is available under the "Exit Today" scenario, the re-rating opportunity is limited, and the certainty of current value is more attractive than the risk-adjusted conditional upside story.

Questions worth pressure-testing:

Is this cybersecurity subsector expected to benefit from meaningful tailwinds such as regulatory or strong acceleration in threat-environment? — or is it largely matured?

Is there a credible buyer universe above £130m, or do most acquirers cluster below £100m?

Are there PE funds actively deploying into this type of business at acceptable multiples?

If the most natural acquirer walks away today, who is next — and on what timeline?

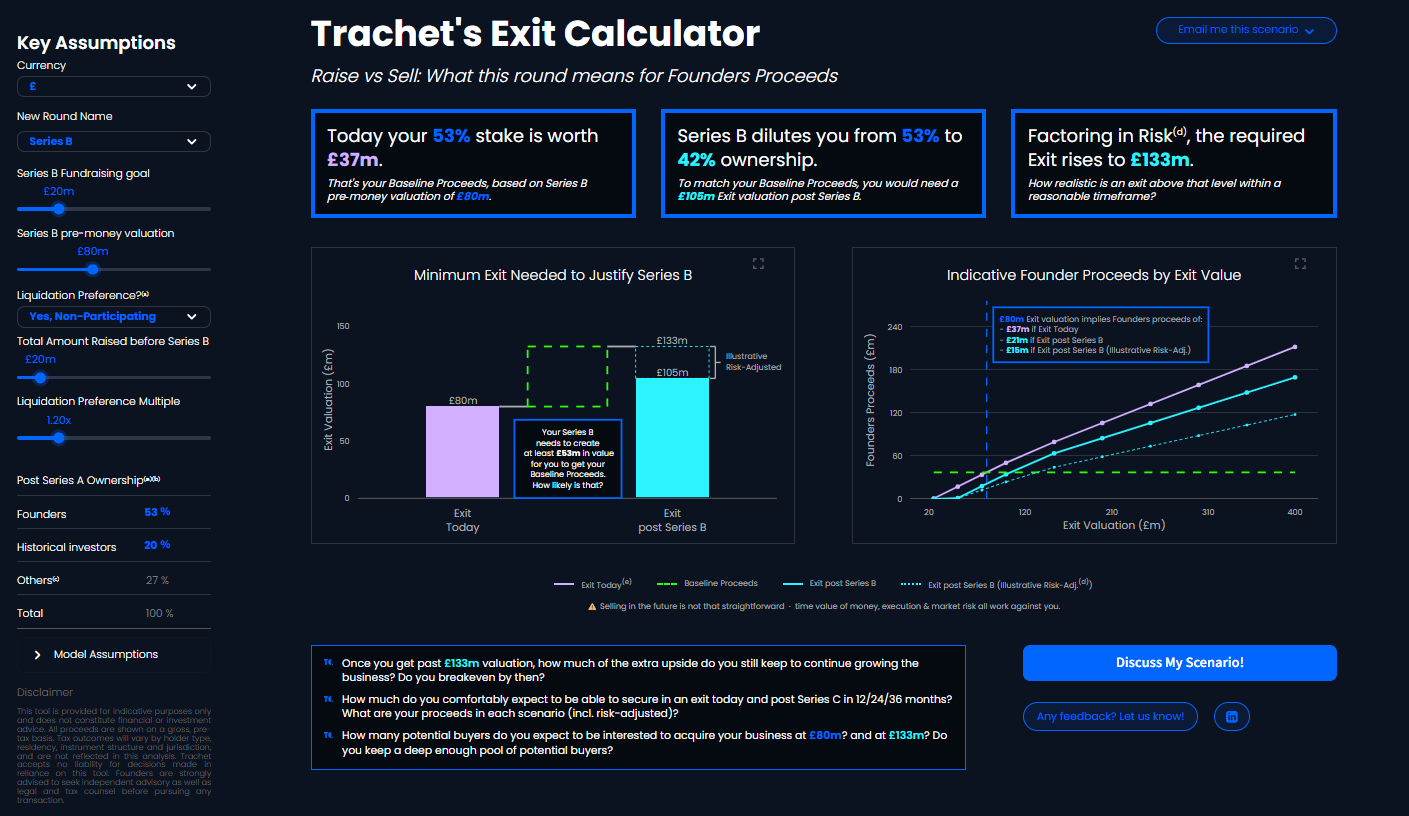

Scenario 2:

Company Y is similar to Company X but post Series A

Company Y is contemplating a Series B and raised £20m to date. There would also likely be buyer interest at around £80m today, but the Board believes that figure reflects the company's current revenue base more than the broader value of what has already been built. The core product has good traction, a second product line and new market motion are showing early promise - but neither is yet at full PMF, and that progress is not yet visible in the reported metrics that buyers use to anchor valuations.

In the calculator, that translates into a similar picture to the prior Scenario 1. With founders being earlier in the journey, their ownership is slightly higher at 53% in this Scenario 2, and their stake is worth £37m today under the "Exit Today" scenario (ie based on the Series B pre-money valuation of £80m). If Company Y raises a £20m Series B instead, founders' ownership reduces from 53% to 42%. On a simple ownership basis, the business needs to reach £105m under the "Exit post Series B" scenario just for the founder to stand still versus their "Exit Today" Baseline Proceeds - a similar level to Scenario 1.

This is where the story matters. The next 12–24 months do have the potential to create a genuine re-rating in buyer appetite. The core product is understood, but the company is still early in converting that technical credibility into broader commercial proof: more contracted ARR, more repeatable enterprise deployments, stronger evidence that it can win beyond its initial customer set. The next phase is not simply "more of the same" - it is the period in which Company Y can move from being viewed as an interesting product to a scaled strategic asset. If hitting those milestones moves the business into a buyer pool that can underwrite £105m/£130m+ outcomes, the "Exit post Series B" path is worth taking. If the likely buyer set still clusters around today's valuation range, the argument weakens - though it may still hold.

Once execution risk is reflected in the calculator, the picture still supports raising — because the upside case is tied to identifiable milestones rather than vague ambition. Company Y is not relying on a speculative market reopening or a dramatic category shift. It is relying on converting work already done into clearer commercial proof points. Even after a sensible risk adjustment, the expected "Baseline Proceeds" remain attractive if management has strong confidence in the 12–24 month plan.

This is the classic case where raising is preferable: the market is under-pricing the asset today under the "Exit Today" scenario, the re-rating opportunity is real, and the additional capital is being deployed against clear milestones that can support a superior exit narrative later.

Questions worth pressure-testing:

Is this cybersecurity subsector likely to face headwinds such as regulatory or budget constraints over the next 12–24 months?

Are the new product lines and geographies close enough to PMF to broaden the pool of potential buyers?

Is there a credible path to building a buyer universe above today's valuation range - or is the argument resting on hoping for a better market?

If the Series B milestones are not hit within 18 months, what is a realistic valuation expectation at that point?

News Roundup

Your go-to monthly roundup of Trachet in the news, key deals in the UK/EU startup arena, and emerging trends to watch.

Trachet in the news

→ Volatility & uncertainty has changed narrative around IPOs - CNBC

CEO Claire Trachet presents Trachet’s views of the IPO market and VC-Backed exits.

→ How geopolitics is influencing investment - City AM

Geopolitics is increasingly shaping investment dynamics, particularly in AI, where governments are both accelerating funding and tightening control. As Claire Trachet argues, the UK’s classification of AI as critical national infrastructure - alongside defence and energy - has introduced a new layer of political risk into the innovation pipeline, with heightened scrutiny over ownership, partnerships, and acquisitions. While investment into UK AI continues to surge, backed in part by significant public funding, this creates a paradox: the state is acting as both a major investor and a gatekeeper. The result is a more complex dealmaking environment where capital is available, but strategic control, national security considerations, and long-term geopolitical positioning are becoming just as critical as financial returns.

→ How The Iran War Is Reshaping Valuations And Investor Expectations - Forbes

The escalation of the Iran war has triggered a fundamental shift in startup valuations, with investors moving decisively away from growth-at-all-costs toward resilience, operational discipline, and cash predictability. As Claire Trachet highlights, investors are now stress-testing businesses against severe downside scenarios—factoring in revenue drops of up to 40% and increased working capital needs—while placing far greater emphasis on supply chain diversification, contingency planning, and near-term ROI. Startups that can clearly demonstrate these fundamentals are maintaining or even enhancing their value, while those reliant on fragile global logistics or optimistic projections are facing early valuation discounts; in this environment, volatility is acting as a filter, rewarding prepared, disciplined founders and exposing weaker business models.

What we’ve been reading

→ Entrepreneurs First crowned a unicorn following $200m fundraise - Sifted

Entrepreneurs First reaches unicorn status after raising $200m at a $1.3bn valuation, with its startup portfolio now valued at $16bn, up from $3bn in 2022. Relocating founders to Silicon Valley has accelerated growth, with many EF startups raising $2–3m seed rounds within days thanks to closer access to US customers, investors and faster fundraising processes. Europe still lags the US startup ecosystem, according to CEO Alice Bentinck, who argues Silicon Valley’s speed, ambition and investor engagement remain far ahead of Europe’s more cautious VC environment.

→ French Health Startup Alan Valued Above €5 Billion After Raise - Bloomberg

French health-insurance startup Alan raised €100m+ at a valuation above €5bn, with the round led by existing investor Index Ventures and participation from Greenoaks, Kaaf Investments, SH Capital and Belfius. The company has reached operational break-even in France and €785m in annual recurring revenue, targeting €1bn ARR this year as it expands its integrated digital health platform. Founded in 2016, Alan is evolving beyond insurance into a broader healthcare platform, combining insurance products with digital services and clinician access.

→ SPACs are back. This time they can’t be a dumpster fire for European startups - Sifted

SPACs are re-emerging in Europe, with quantum companies IQM and Pasqal planning public listings via SPAC mergers, signalling renewed interest in the structure after the troubled 2021 wave. Deeptech companies are turning to SPACs due to Europe’s funding gap, as raising the hundreds of millions needed for sectors like quantum computing remains difficult beyond Series B. The success or failure of these listings could shape Europe’s tech sovereignty ambitions, as capital-intensive sectors like AI, quantum and defence increasingly depend on public markets to scale.

→ PitchBook | Record European private debt fundraising signals shift in global capital allocation

European private debt fundraising reached $79.4bn in 2025, up nearly 40% year-on-year, giving the region a record 33.9% share of global private debt capital. North America’s dominance is slipping slightly, with its share of global fundraising falling from 71.9% to 63.3%, as investors seek diversification and higher spreads in Europe. Direct lending is driving the growth, supported by tighter bank lending regulations and large vehicles such as Ares’ €17.1bn fund and CVC’s €10.4bn fund, signalling stronger institutional demand for private credit in Europe.

We’re keen to hear about the key challenges (or opportunities!) shaping your company’s objectives in 2026. Email me at claire@trachet.co for more information on topics you'd like to see discussed in future issues of What’s the deal?