What's the deal? The Tech M&A & Fundraising Newsletter - Is time on your side?

For much of the last decade, time worked in founders’ favour. The “J curve” allowed companies to reasonably have time on their side to scale, for their markets to mature and tailwinds to kick-in - and as a result, for their valuations to increase. However, the last couple of years have put that assumption under strain. Liquidity remains constrained and recent VC fundraising figures signal this is likely to worsen, exits are concentrated in M&A, and risk seems to accumulate faster than value compounds.

Welcome to What’s the Deal? - your monthly deep dive into the strategic currents defining the tech investment landscape.

This edition focuses on Is time on your side? and examines why waiting no longer reliably improves exit and fundraising outcomes, why 2026 may offer a narrower but more actionable window than in 12-24 months’ time, and what founders should be pressure-testing now to preserve leverage and optionality.

A note from the Editor - CEO Claire Trachet

"For a long time, waiting was a rational strategy for startups. Time allowed companies to scale, markets to mature and tailwinds to play out, often supporting valuation growth along the way. Optionality increased simply by staying in the game a little longer, as long as founders had enough cash to execute their plan.

"That logic no longer holds as clearly. In today’s market, waiting does not reliably translate into higher valuations once risk and inflation are taken into account. Risk now declines more slowly than in the last cycle, while inflation continues to erode real outcomes. Across both fundraising and M&A, there is little evidence of a structural premium for waiting. Longer timelines are increasingly delivering flat nominal valuations - and lower ones in real terms - while negotiating positions weaken as cash tightens and perceived differentiation fades.

"The data reflects this shift. The journey from a first VC cheque to a Series B in Europe now averages close to six years, compared to around four years before 2020. More time increasingly means more exposure - not just to execution risk, but to external risks founders cannot control.

"Capital is also more selective, not because ambition has disappeared, but because liquidity is constrained. European VCs raised just €9.3bn in 2025, nearly 60% below last year and more than 70% below the 2022 peak. Fewer funds are active, fewer cheques are written, and growth capital is available only for a narrow set of companies. In this context, time no longer expands optionality by default.

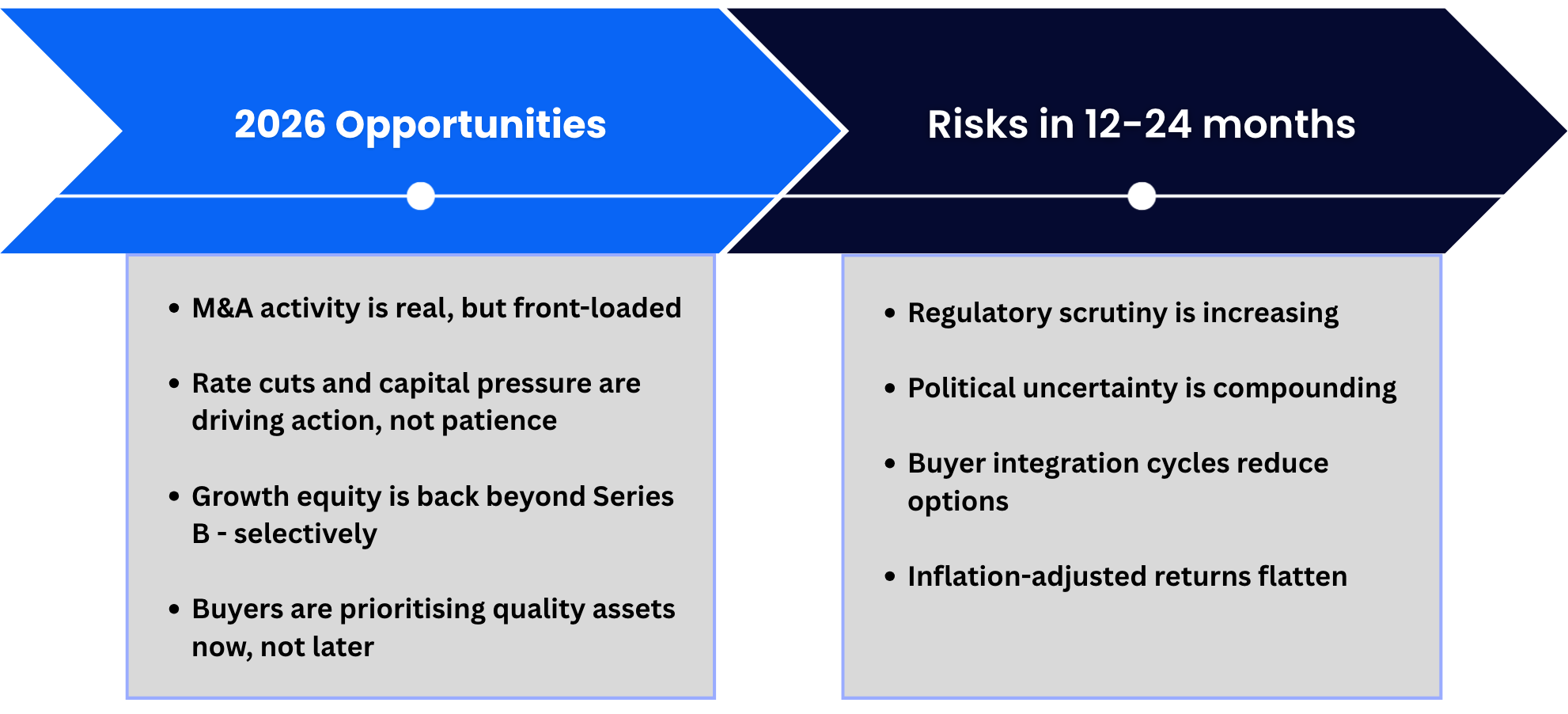

"This is why 2026 matters. Over the next 12–24 months, volatility is more likely to increase than recede - from geopolitical instability and trade uncertainty to more interventionist governments and tighter regulatory scrutiny ahead of election cycles. At the same time, buyers are operating within integration and capital constraints, making M&A more defensive and capability-led. This creates windows, not long runways - with 2026 emerging as a narrower but more actionable one.

"This is not an argument for selling too early. Europe needs strong, independent champions, and founders - alongside investors - should remain ambitious and focused on building enduring businesses. But it is also an advisor’s role to assess, realistically, whether time is genuinely compounding value, or quietly extending risk. In the current environment, acting deliberately in 2026 may preserve more leverage than waiting into 2027 in the hope that conditions improve.

Why does 2026 matter for M&A?

“That said, we’re excited to see constructive M&A discussions as the year begins. The deep dive below sets out a simple pressure test to help assess whether waiting is genuinely compounding value, or quietly extending risk.

Is time on your side?

A quick pressure test for founders

Founders rarely think about timing as inactivity. Most are executing hard - building, selling, hiring, shipping. The real question is not whether you are moving fast, but whether time itself is improving your leverage in terms of fundraising and M&A - or quietly eroding it

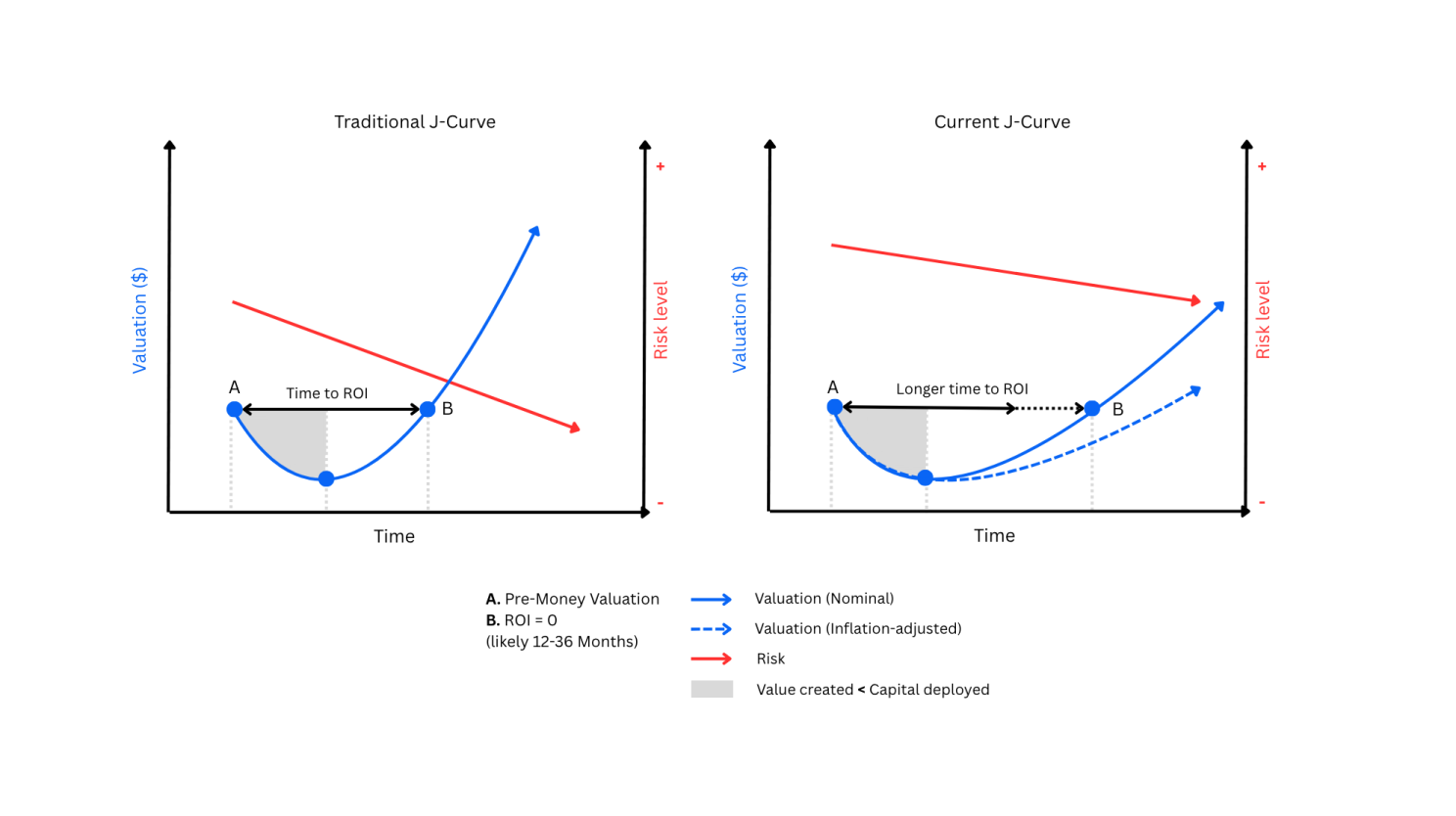

Trachet: Traditional J-Curve vs Current J-Curve

The two charts above illustrate how the role of time has changed.

The first shows the traditional J-curve, where risk fell quickly as value compounded.

The second shows today’s reality, where risk falls more slowly, valuation growth is uneven, and inflation can erode real outcomes.

Together, they explain why timing is no longer neutral - and why it needs to be pressure-tested.

Pressure test 1: Does time still improve your outcome?

Historically, time worked in a founder’s favour because uncertainty resolved faster than value compounded. Risk declined steeply, valuation accelerated, and the gap between the two widened. Today, that divergence is weaker.

In many cases:

Nominal valuation rises slowly

Inflation erodes real value

Risk declines, but not fast enough to compensate

Pressure test:

Once risk and inflation are considered, what is the specific mechanism by which waiting 2–3 years improves your outcome?

What are the real benefits of time - and what are the hidden costs?

(If the answer is vague, time is not doing the work you think it is.)

Pressure test 2: What actually changes if you wait?

(Growth and execution reality)

The long game has become harder. Growth no longer compounds automatically. Sustained 40–50% growth is strong - but step-change acceleration (150–200%) is rare. Competitive advantages are copied faster, particularly in SaaS and AI. Roadmaps alone don't necessarily buy valuation unless execution is immediate and visible.

Pressure test

What specifically changes your leverage in the next 12–24 months?

Which milestones genuinely shift buyer perception - and which simply extend the timeline?

(Waiting only works if something material changes.)

Pressure test 3: How buyers actually behave

(Why windows matter)

M&A today is driven less by optimism and more by necessity. Buyers are acting defensively, constrained by integration capacity, regulatory scrutiny and capital allocation cycles. This creates windows, not long runways.

Pressure test

If a buyer does not act now, are they likely to act later - or integrate elsewhere?

What would need to change for their answer to be different?

(Assuming buyers will “come back later” is often the wrong default.)

Pressure test 4: When waiting deserves scrutiny

Waiting deserves closer examination when:

Execution has missed expectations

Runway is limited

Outcomes depend on a single future milestone resetting perception

Pressure test

Is waiting expanding your options - or simply postponing a decision?

What prevents preparing a dual-track that protects downside while preserving upside?

Who is actively challenging this assumption - you, your board, or no one?

(Stubbornness builds companies. Blindness destroys them.)

A simple decision lens

Clear near-term execution and momentum? Time may still work in your favour.

Differentiation buyers can’t build? Earlier engagement may preserve leverage.

Weak traction and limited runway? Time is unlikely to change the equation on its own.

Trachet Deal Roundup

Saporo closes €7M Series A to scale its graph-native identity security platform

In December 2025, Trachet advised Saporo, Switzerland’s fastest-growing startup (Sifted 250), on its €7m Series A - a fully pan-European round backed by investors from five countries as the company expands across France, Switzerland, Benelux, Germany and Italy, with selective US growth.

The round was led by TIN Capital, with participation from Giesecke+Devrient Ventures, CDP Venture Capital, XAnge, Lightbird VC and Session VC, combining capital with deep strategic reach across Europe’s cybersecurity ecosystem.

Saporo CEO, Olivier Eyries said:

"Trachet is a trusted voice - by us co-founders and the Board alike - and brought Saporo to a new level in terms of reasoning and planning. A true partner, like an extension to Saporo. Thanks to their support and resilience at every step, we approached investors with far more confidence, which helped us secure strong terms.”

News Roundup

Your go-to monthly roundup of Trachet in the news, key deals in the UK/EU startup arena, and emerging trends to watch.

What we’ve been reading

→ Inside Hiro Capital's €500m plan for European startups: ‘We can shift the dial’ – Sifted

Sifted reports that Hiro Capital’s planned €500m fund is explicitly targeting the post–Series B “valley of death”, where European startups struggle to access patient capital. The signal is less about fund size and more about timing: without credible late-stage pathways, founders are pushed into premature exits or US-led financings. Hiro’s thesis reframes growth capital as strategic infrastructure — linking scale-up funding to European tech sovereignty, execution discipline and the ability to remain independent for longer.

→ UK maker of AI avatars nearly doubles valuation to $4bn after funding round-The Guardian

UK-based AI video startup Synthesia nearly doubled its valuation to $4bn after raising $200m in a round led by existing investor Google Ventures, underscoring how capital continues to concentrate around proven AI platforms. The company, which counts 70% of the FTSE 100 as customers, generated $58m in revenue in 2024 and expects to reach $200m this year, despite remaining loss-making as it invests heavily in product and headcount. The round was led predominantly by insiders, signalling that in AI, scale, distribution and repeat usage - not hype - are now the clearest drivers of valuation support.

→ Nvidia's backdoor acquisition won’t be the last – Bloomberg

Bloomberg highlights how US companies spent $37bn on generative AI software in 2025, up from $11.5bn the year before, with acquisitions increasingly structured to minimise regulatory scrutiny. The signal for founders isn’t just consolidation, but how it’s happening: quietly, quickly and often without competitive processes. Big Tech is prioritising speed and control over visibility, reinforcing why waiting for a headline-grabbing exit is increasingly misaligned with buyer behaviour.

→ The startup-on-startup M&A spree is not slowing down – Pitchbook

PitchBook data shows that startup buyers accounted for 38.4% of all M&A involving US VC-backed companies in 2025, the highest share on record. Of 1,009 VC-backed acquisitions, 387 featured venture-backed acquirers, contributing $31.1bn of the $139bn total deal value. The trend reflects a maturing ecosystem where well-capitalised scaleups are using M&A to consolidate fragmented markets, secure talent and capabilities, and build IPO-viable platforms as the public markets’ revenue bar rises sharply - now estimated at $500m+, up from ~$150m pre-2021. For founders, the signal is clear: exits are increasingly intra-ecosystem, competitive, and time-bound, with fewer companies graduating independently to the public markets.

→ The top VC predictions for Europe in 2026 – Sifted

In its 2026 outlook, Sifted captures a broad investor consensus: capital will continue to concentrate as liquidity pressure rises, leaving smaller managers and recent vintage startups exposed. VCs warn that many companies funded in 2023–24 on aggressive growth assumptions face funding risk due to weak retention and profitability, accelerating down rounds, consolidation and forced exits. AI remains foundational, but most agentic startups are expected to wash out, while defence tech hype cools as procurement realities bite. Timing, not ambition, is becoming the decisive factor.

→ UK business confidence drops to 3-year low, survey shows– Reuters

Reuters reports UK business confidence fell to its lowest level since 2022 at the end of 2025. For founders, the relevance is not sentiment alone, but impact: lower confidence feeds longer sales cycles, slower investment decisions and tighter scrutiny — increasing the opportunity cost of waiting in already constrained markets.

→ Lessons learnt are key to making a success of acquisitions – The Times

Writing in The Times, Simon Morrish argues that most acquisitions fail not because of deal logic, but because founders and boards underestimate post-deal execution. Integration, leadership capacity and operational focus - not capital - are the binding constraints. For founders considering M&A, this reinforces why buyers are selective and windows are short: acquirers will only move when they believe they can absorb and improve what they buy.

We’re keen to hear about the key challenges (or opportunities!) shaping your company’s objectives in 2026. Email me at claire@trachet.co for more information on topics you'd like to see discussed in future issues of What’s the deal?