What's the deal? The Tech M&A & Fundraising Newsletter - Investor Relations 1o1

Investor Relations 101

European tech continues to create value at scale. But as VC fundraising tightens and liquidity becomes a sharper concern for LPs, turning that value into realised outcomes has become harder - particularly for companies outside the very top tier.

Welcome to What’s the Deal? - your monthly deep dive into the strategic currents defining the tech investment landscape.

This month's edition focuses on Investor Relations as a leadership discipline across the full company lifecycle - before, during and after fundraising or M&A - and why disciplined IR has become central to preserving optionality, especially for middle-of-the-pack companies.

A note from the Editor - CEO Claire Trachet

“As we close out 2025, it’s tempting to tell the story of European tech through the headlines: AI capital concentrating into fewer, larger rounds; sectors like deeptech, fintech and defence pulling investment timelines forward; and a return of high-profile “mega deals” - such as Mistral AI’s €1.7 billion Series C and Nscale’s $1.1 billion Series B - signalling high confidence at the very top of the market.

“There is real progress behind those headlines. Europe’s tech ecosystem has expanded rapidly over the past decade and now sits close to $4tn in value, with more than 400 billion-dollar companies built across the continent. The ability to create value is no longer in question.

“What continues to matter and create concern is how consistently that value is realised, and how this will continue to impact the ecosystem going into 2026.

"Below the headline deals, conditions are tightening. European venture funds have raised significantly less capital year-on-year, compressing reserve capacity and raising the bar for follow-on support.

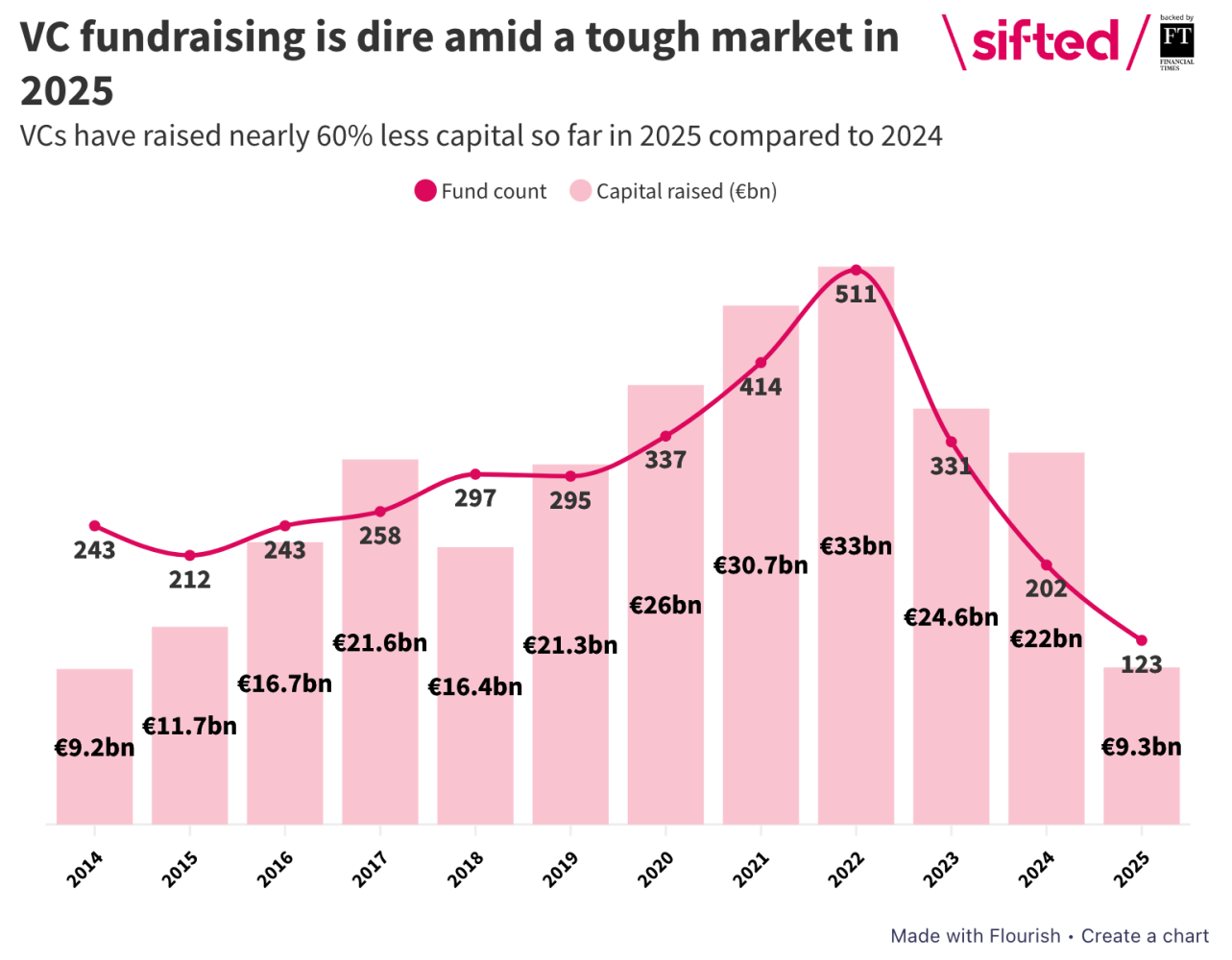

Source: Sifted - European VCs have raised nearly 60% less funding in 2025 (sifted.eu/articles/european-vc-fundraising-2025-down)

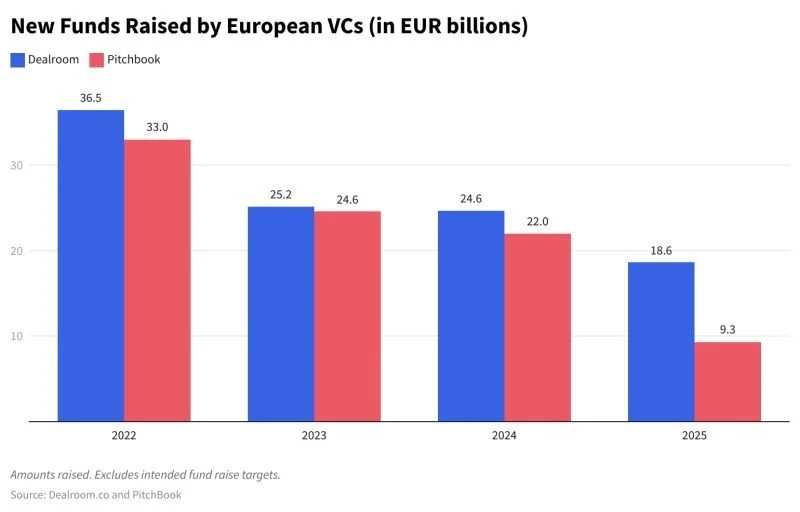

Different datasets point to different degrees of severity. While PitchBook figures reported by Sifted suggest European VC fundraising is down close to 60%, Dealroom.co data points to a more moderate contraction of around 25% - however most importantly their data show a clear reshuffle within Europe. As highlighted by Dealroom CEO Yoram Wijngaarde, UK fundraising is down roughly 56% year-on-year, while France has overtaken the UK, reaching an all-time high.

Different datasets point to different degrees of severity. While PitchBook figures reported by Sifted suggest European VC fundraising is down close to 60%, Dealroom.co data points to a more moderate contraction of around 25% - however most importantly their data show a clear reshuffle within Europe. As highlighted by Dealroom CEO Yoram Wijngaarde, UK fundraising is down roughly 56% year-on-year, while France has overtaken the UK, reaching an all-time high.

The common signal is not a collapse of capital, but tighter reserves, greater selectivity, and less margin for error. Stakeholders on deals are particularly tensed this season, even on deals well progressed and with strong outcomes.

"At the same time, figures circulating widely on LinkedIn - attributed to remarks by Alfred Lin at Sequoia Capital - suggest that even top-performing funds write off roughly half their portfolios. The exact percentage matters less than the structural reality it reflects.

“Across Europe, a large cohort of Series A and beyond companies now sit between early-stage optionality and breakout scale. They have real revenue, customers and teams, but no longer fit a power-law narrative. We call these the middle-of-the-pack of the tech startup ecosystem. They won’t return a fund on their own - but handled deliberately, they can lift overall fund performance by 20% or more, help address liquidity pressures, and deliver meaningful outcomes for founders and backers.

“These companies sit at a strategic crossroads. Performing well enough to not be seen as a lost cause, yet not seeing enough momentum to have an obvious path to the next fundraising or an exit. Their outcomes depend greatly on whether optionality is engineered early - across capital structure, governance, buyer logic and timing to navigate this rough period and make the most of the next few cards the company will be dealt with. For founders in this position, Investor Relations becomes a leadership discipline. Not just as a reporting exercise, but as the mechanism that keeps momentum visible, shareholders aligned and strategic options open.

“This month’s Deep-Dive explores Investor Relations from Series A onwards, and how maturing this discipline early helps convert execution into realised outcomes.”

Investor Relations 101 - Series A and Beyond

From Series A onwards, Investor Relations shifts from storytelling to increasingly using the numbers to maximize real/tangible optionality.

For companies in the middle-of-the-pack, IR is one of the few disciplines that directly shapes external outcomes founders don’t otherwise control - investor confidence, follow-on support, governance alignment and strategic timing. Done well, it preserves speed and agility. Done poorly, it quietly narrows the range of viable paths.

At this stage, IR becomes stewardship: of data, trust and decision-making discipline. Compounded over time, it lowers the cost of capital, strengthens board dynamics, and materially improves both the odds and outcomes of any potential fundraising or M&A.

Pre-Fundraising or M&A: intentional differentiation of IR vs Board

Confusion between IR and governance is extremely common - and easily foresaken in founder-friendly environments. The Board typically has people representing the different classes of shareholders, and investors use monthly/quarterly updates and ad-hoc calls to get the level of information they need on run-rate.

In tighter markets, that confusion undermines momentum - which becomes costly: the pace accelerates, investors lose visibility, boards get dragged into operational detail, and decision-making slows just when speed and clarity matter most.

So, unless you're in the top 10% performing companies of your investor's portfolios (in which case you probably already do some version of the below), start intentionally differentiating:

Board management: this is about governance and decisions. Quarterly meetings should focus on trade-offs, capital allocation, and strategic direction. Keep in mind that the Board has a mandate to run the company on behalf of all the shareholders - that's the "fiduciary duty" meaning the Board members do not act for the fund they represent but for the best interest of the company.

Investor Relations: this is about maintaining momentum and alignment across all shareholders. It is the narrative of execution: KPIs, progress against plan, risks, and specific asks - but most importantly Relationship strengthening. So that when quick decisions need to be made - especially a tough call - that relationship is warm and resilient: investors are empowered to take intelligent decisions, quickly.

Separating the two ensures investors stay informed and supportive, while boards remain effective decision-makers.

During the Deal: Momentum is Currency

The European venture market in 2025 is less harsh than last year, yet it is not founder-friendly. The companies that can show best-in-class momentum still get good deals - even if not easily - and the rest may struggle. Transactions' successful closing are increasingly becoming hypersensitive to process and timely progress.

A signed Term Sheet is not money in the bank - it is a milestone that requires discipline to convert. Even for the best companies, in current times, there are sometimes tough calls to make on short notice. You need to speak to your historical investors very regularly throughout the process, to ensure you can navigate the turbulences efficiently - ie as a team.

Momentum should be made visible both to Historical investors and new investors:

Historical investors: keep them emotionally invested in this fundraising, independent of how much they re-invest. Their support can be critical if tensions arise during the process, and the relationship capital will remain valuable well beyond this round.

New investors: while dataroom & due diligence are focused on fact-checking (ie. be well organised, be upfront, clear and concise), IR is your chance to drip-feed good news to keep the investors excited. Ensure you keep these good news coming throughout the transaction about your trading performance, your R&D or even broader market developments.

Running an effective IR is very time-consuming during a fundraising process - and it arguably is the #1 job of a CEO. Get your advisor and your team to run the dataroom and the due diligence discussions, and ensure you don't solely focus on the mandatory Board updates (ie the Governance aspect) and instead leverage those critical weeks to strengthen your relationships with your investors - "old and new".

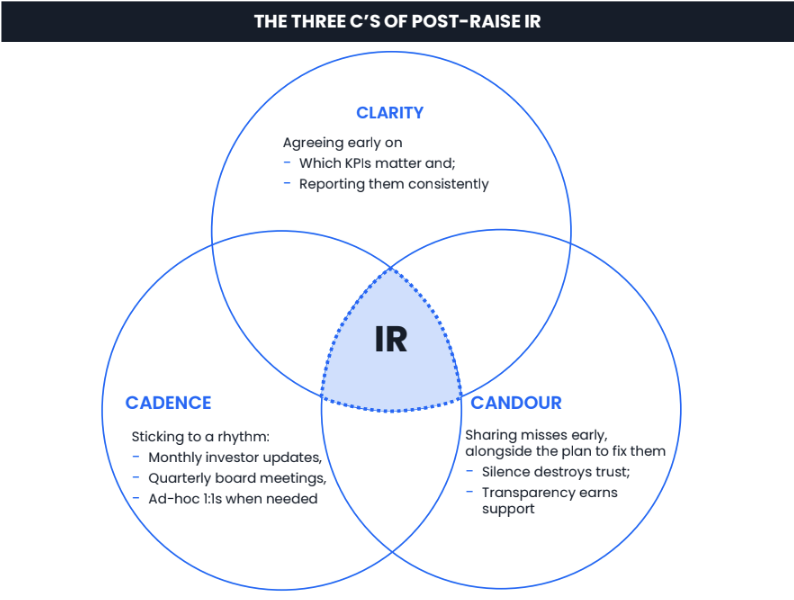

The three C’s of Post-Raise IR

Post-raise, continue building on your momentum. Nobody wants to hear that when tired after a raise, yet that's a very efficient way to build relationship capital for when needed - whether times get tough or a decision needs to be taken fast that doesn't make clear unanimity. Your future self will thank you for not dropping the ball post your fundraising.

As portfolios mature and reserve capital tightens, investors look for three signals that a company is being run with discipline: Clarity on what matters, Cadence in how progress is communicated, and Candour when reality diverges from plan. IR is the way to score on these three over time, so you can convince investors to make the intelligent decision you need to when it comes.

The framework above shows how effective investor relations sits at the intersection of these three disciplines - and why IR breaks down when even one is missing.

Each of these practices reinforce one another, IR eventually becomes a system rather than a set of updates.

Investor Relations is a leadership discipline. It is how you convert execution into optionality and how you can navigate favourably in all weather - whether that translates into raising on better terms or exiting from a position of strength. Keep the line clear between IR and Board, maintain cadence and clarity, and above all, make momentum visible.

News Roundup

Your go-to monthly roundup of Trachet in the news, key deals in the UK/EU startup arena, and emerging trends to watch.

Trachet in the news

→ Story Over Numbers - Entrepreneur

Claire Trachet argues that while fundraising has always required strong vision, the last cycle exposed the cost of letting narrative outrun evidence - a risk now resurfacing in parts of the AI ecosystem. The 2020–21 boom saw valuations surge as diligence collapsed, forecasts weaken and pre-revenue rounds become the norm; when markets corrected, down rounds spiked, KPIs were restated and board confidence eroded rapidly, with very few companies ever recovering credibility enough to achieve strong exits. While discipline has returned, AI is again seeing capital deployed before validation, with ambition preceding sequencing rather than evidence.

→ Saporo closes €7M Series A to scale its graph-native identity security platform - Tech.eu

Swiss cybersecurity startup Saporo has raised a €7m Series A round led by TIN Capital, with participation from G+D Ventures, CDP Venture Capital, XAnge, Lightbird VC and Session VC. Trachet advised Saporo on the transaction, supporting the company as it scales across Europe and the US amid rising demand for identity-led security solutions.

What we’ve been reading

→ European VC fundraising has fallen off a cliff in 2025 - Sifted

Anna Sraders reports that European VCs have raised just €9.3bn so far this year - nearly 60% down on 2024 and over 70% below 2022’s peak - with only 123 funds closed versus 202 at this point last year. The punchline isn’t just “cycle”; it’s liquidity. Without exits and distributions, LPs are cash-constrained and increasingly unwilling to re-up - leaving anyone without a top-tier brand or a clear edge fighting for oxygen.

→ AI is pulling tech M&A into record territory - Bloomberg

Bloomberg News says global tech dealmaking has hit $1tn in 2025, powered by an AI land-grab: buyers are chasing data infrastructure, cybersecurity, GenAI tooling and data centres, with a “don’t get left behind” psychology dominating. The signal for founders: strategic M&A appetite is real - but it’s clustering around assets that make AI deployments safer, faster, and cheaper (and around companies that own distribution).

→ Anthropic is already being framed as the next blockbuster IPO - The Times

Louisa Clarence-Smith reports Anthropic is preparing for a potential IPO as early as 2026, with private valuation chatter ranging from $183bn to $300bn+ amid the enterprise AI race. Notably, even the “credible” leaders are openly warning about YOLO-style risk-taking - a clue that we’re moving from optimism into late-cycle behaviour (where everyone is bullish, but nobody wants to be last holding the bag).

→ The Bank of England is now treating AI valuations like a stability risk - Reuters

Reuters reports the BoE flagged inflated AI-related valuations as a meaningful threat: if sentiment turns, the correction could leak into credit markets - especially as AI firms become more intertwined with lending. It also highlighted the gilt-repo leverage build-up (near £100bn) as a fragility point if refinancing dries up. Translation: the UK’s “risk” isn’t just startups - it’s the plumbing around them.

→ Lovable’s latest round reportedly prices it at $6.6bn - CNBC

CNBC reports (via an RSS-republished feed) that Swedish “vibe coding” startup Lovable is raising at a reported $6.6bn valuation, with Accel participating, underscoring how aggressively capital is still chasing breakout AI distribution + usage curves - even as regulators warn about bubble dynamics elsewhere. The Europe angle is sharp: when European VC fundraising is shrinking, a handful of AI-native winners are still able to command US-style pricing.

→ Fintech consolidation watch: Mollie buys GoCardless for €1.1bn - Financial Times

The FT reports Dutch payments group Mollie has agreed to acquire UK fintech GoCardless in a deal aimed at creating a roughly €3bn European payments leader. This is the “Europe can still build champions” version of M&A: combine profitable rails, broaden product surface area, then scale internationally - instead of selling early to the US.

We’re keen to hear about the key challenges (or opportunities!) shaping your company’s objectives in 2026. Email me at claire@trachet.co for more information on topics you'd like to see discussed in future issues of What’s the deal?