What's the deal? The Tech M&A & Fundraising Newsletter - The Founder’s Guide to M&A

The Founder's Guide to M&A

European tech continues to create value at unprecedented speed, yet value realisation is slowing sharply. IPOs have collapsed, M&A now accounts for nearly all exits, and liquidity is recycling far more slowly than the market was built for. Founders face a landscape where fundraising is no longer enough - strategic pathways must be engineered early.

Welcome to What’s the Deal? - your monthly deep dive into the strategic currents defining the tech investment landscape.

This edition focuses on The Founder’s Guide to M&A and examines how founders can design credible liquidity pathways, navigate exit timing, and build optionality long before the market is ready to deliver an outcome.

A note from the Editor - CEO Claire Trachet

“This month has shown just how far Europe’s tech ecosystem has come. Atomico’s 2025 “State of European Tech” report highlights a continent now home to more than 400 unicorns, with founders building stronger, faster and with deeper technical and commercial maturity than at any point in the past decade. The recent wave of activity - Lovable at $6.3bn, Fuse Energy at $5bn, Vintedpreparing for €8bn, and Revolut’s secondary at a $75bn valuation - only reinforces how powerful Europe’s value-creation engine can be.

“So today, for founders and investors, the real question is no longer whether Europe can create value. It is whether the ecosystem becomes able to realise that value in a predictable, scalable way.

"And here, the data paints a very different picture.

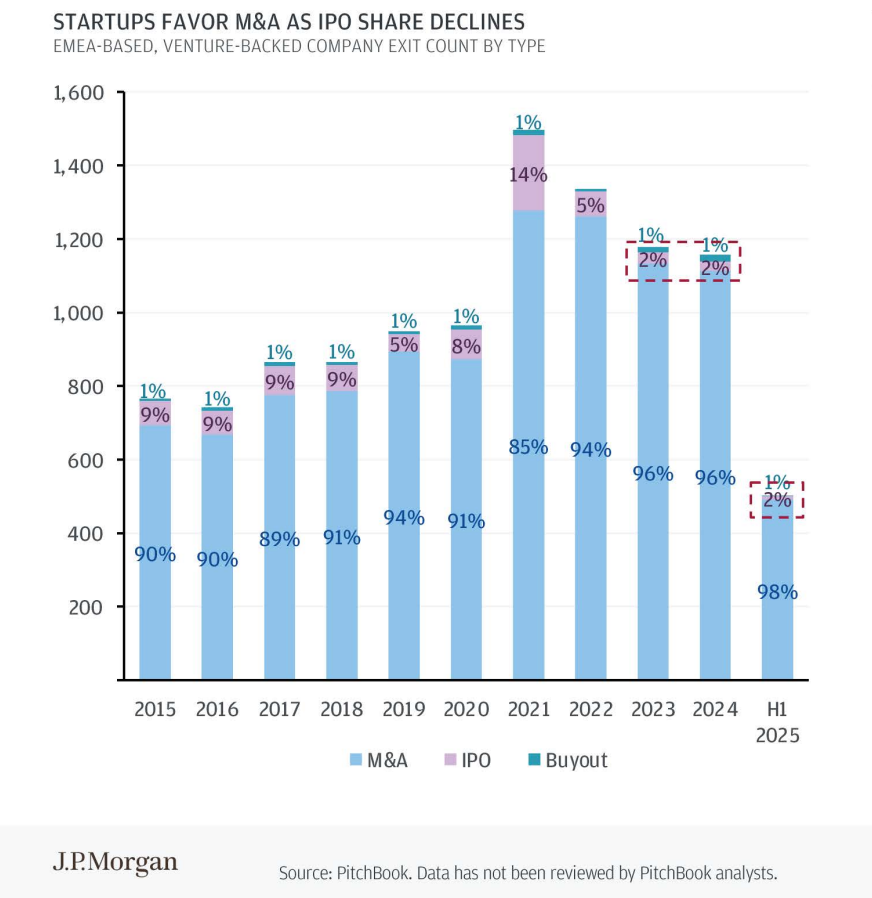

“According to J.P. Morgan’s 2025 EMEA Exit Report, 98% of European VC-backed tech exits in H1 2025 were M&A. Public listings, meanwhile, have collapsed - IPOs now represent just 2% of all exits, down from 14% at their 2021 peak, and materially below the 8–10% range that defined most of the previous decade. These levels mark the lowest IPO share in more than ten years.

“And even within M&A, 51% of transactions fall between $1m-$50m, and 70% are undisclosed, a range at odds with the valuations of most companies’ latest funding round. A study by PitchBook found that From 2022 to 2024, 70% of VC-backed exits were valued at less than the capital investors put in, rising from 58% for the period between 2009 and 2014.

“J.P. Morgan’s data also shows the median time to exit is now exceeding eight years, and US buyers account for 22% of all EMEA acquisitions. When exits do happen, they are disproportionately realised outside Europe.

“For founders, this is an important reminder; fundraising may set a valuation on paper, but the only valuation that truly counts is the one realised at exit - and you cannot assume the market will deliver it for you.”

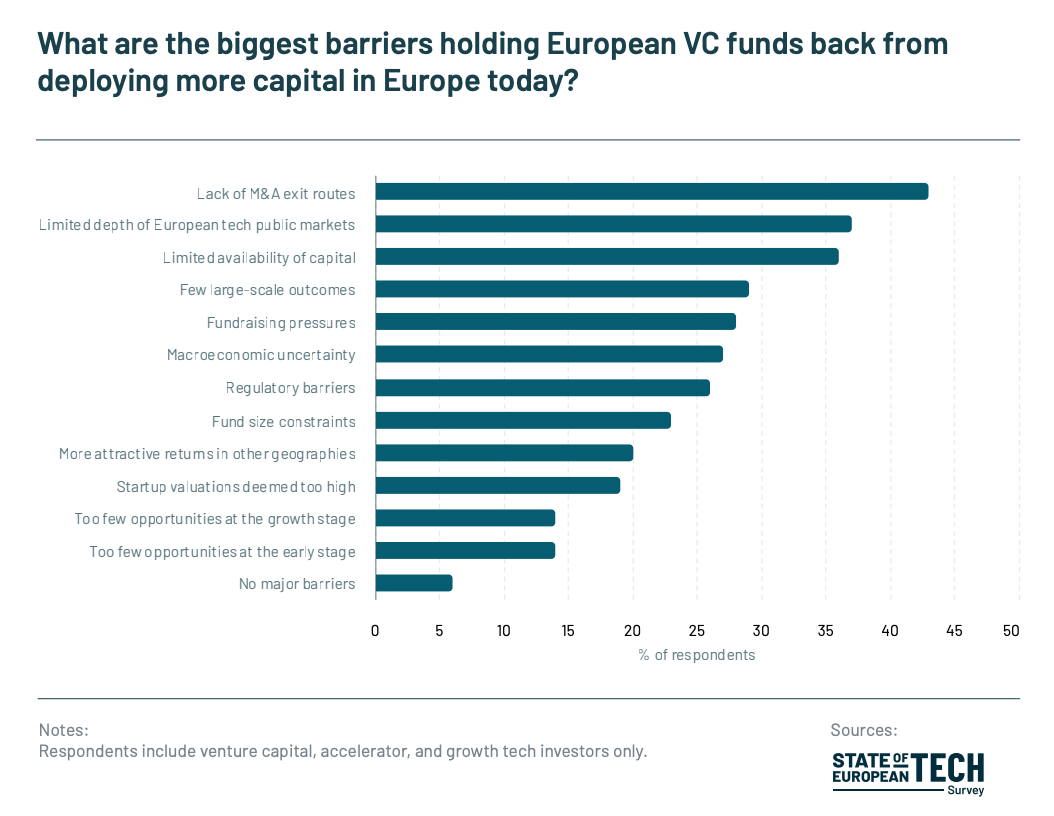

“For investors, it means capital is being locked in for longer, underwriting risk is rising, and realisation pathways need to be planned far earlier than before. Atomico’s research highlights European VC’s biggest concern today is the lack of M&A exit pathways, with approx. 46% of those surveyed saying it is the single biggest barrier to deploying more capital, ahead of valuations, pricing, or opportunity scarcity.

“This dynamic heightens pressure on ‘middle-of-the-pack’ companies - no longer early-stage, but not yet category leaders - where the next strategic decisions determine whether they scale, stall, or consolidate. In earlier cycles, founders could prioritise growth and worry about realisation later; today, the two must be managed in tandem. Atomico’s data signals that investors are expecting greater maturity, not just in product and revenue, but in strategic positioning - with clear buyer logic, integration pathways, and a credible long-term realisation narrative actively present.”

“The answer (in my opinion) is not hoping for a one-off ‘M&A boom’ in 2026. What the ecosystem needs is a deeper, structural change - a mentality where M&A and IPOs are built into company planning early, rather than left to chance.

“This month’s Deep-Dive focuses on exactly what this means for you as a founder and how to design liquidity pathways long before the market is ready to deliver them.

“Because in this environment, those who master both creation and realisation remain what they must be: masters of their destiny."

Understanding Your Exit Routes: A Founder’s Guide to M&A Pathways, Timing, and When Continuing to Raise Makes Sense

1. The Three Primary Exit Routes for Venture-Backed Founders

With 96% of European companies exits now occurring through M&A while IPO activity remains at multi-year lows, most founders scaling through the mid-stages will ultimately navigate a strategic transaction rather than a public listing. Yet, there are several different exit pathways and the mechanics behind them vary - these typically depend on timing, how much you raised to date and your investors’ targets.

Strategic M&A

This is the most common and often most value-accretive outcome. Strategics acquire for acceleration, not optimisation. This can be for faster market entry, product expansion, and defensibility. Acquirors primarily value synergies that are in their control.

When it works:

You bring something a strategic couldn’t yet build successfully/cannot build quickly (ie reducing R&D/Product risk for them)

Your client base complements theirs (ie geographic expansion)

Your revenue quality and cohorts are strong enough to support premium multiples (ie bringing them increased ways to upsell their existing clients)

What to consider?

Strategics tend to be very grounded and heavily discount based on risk of integration. This means you’ll get most value the closer you are to their existing business and you must develop a strong narrative - backed by a solid business case. Strategics typically target 2-3years ROI internally, which you must compete against.

Timing is also critical: too early in your journey and your valuation won’t capture much of the potential of what you’re building as not enough is proven; however past the $300m threshold you’re entering proper “mid-cap” territory - and the rules of the game change.

It is key to discuss regularly with your Board whether your company is on-track to build a stand-alone giant, or whether/when to optimise for an integration with a strategic player. Your ability to articulate a combined strategic value is vital. As a founder, this is a chance to set up a legacy by ensuring your original mission is delivered on a larger scale through the strategic partner's platform and resources.

Private Equity / Expansion Buyout

PE is increasingly active in European tech, particularly in companies with repeatable revenue and clear paths to margin expansion. These acquisitions value discipline as much as growth.

There are five primary levers PE firms use to drive value creation in a portfolio company:

Grow your revenue

Expand your margins

Complete strategic acquisitions

Pay down debt

Expand your exit multiple

When it works:

Growth is stabilising post hyper growth but cash generation is improving

Your category is consolidating

You can demonstrate operational resilience and forward visibility

What to consider?

Buyouts often allow founders to realise some liquidity while still retaining meaningful equity in the business. At this stage, financial maturity becomes critical: clean data, reconciled metrics, and reliable forecasting will materially influence outcomes. A buyout can give founders the chance to participate in the next phase of growth with reduced personal risk - taking some capital off the table while benefiting from the operational discipline that a seasoned private equity partner brings.

So what about Acquihires?

Often presented as an “exit pathway,” but in reality usually a situational outcome. In some (rare) cases, in a very hot market with few qualified resources, it is a way for the larger company to recruit a whole team - and for the founders to be "intrapreneurs". However Acquihires are most common when the business/product can no longer justify a standalone valuation and the team becomes the core asset. It is rarely the path founders imagine at inception, and in many cases is closer to a distressed sale than a strategic one...

When it works

The team is exceptional, but runway is tightening

The buyer values talent or IP more than the business as a whole

It protects equity value that might otherwise compress to zero

It is surfaced proactively, not at the point of failure

What to consider?

A small transaction is not inherently a distressed one! But a distressed process often results in an acquihire... For founders of smaller companies to manoeuvre this tricky path: best to address this with your Board deliberately, early, and with clear expectations. Structured correctly, an acquihire can preserve reputation, protect teams, and be a decent financial outcome for all stakeholders. Structured poorly, it becomes a fire-sale under another name.

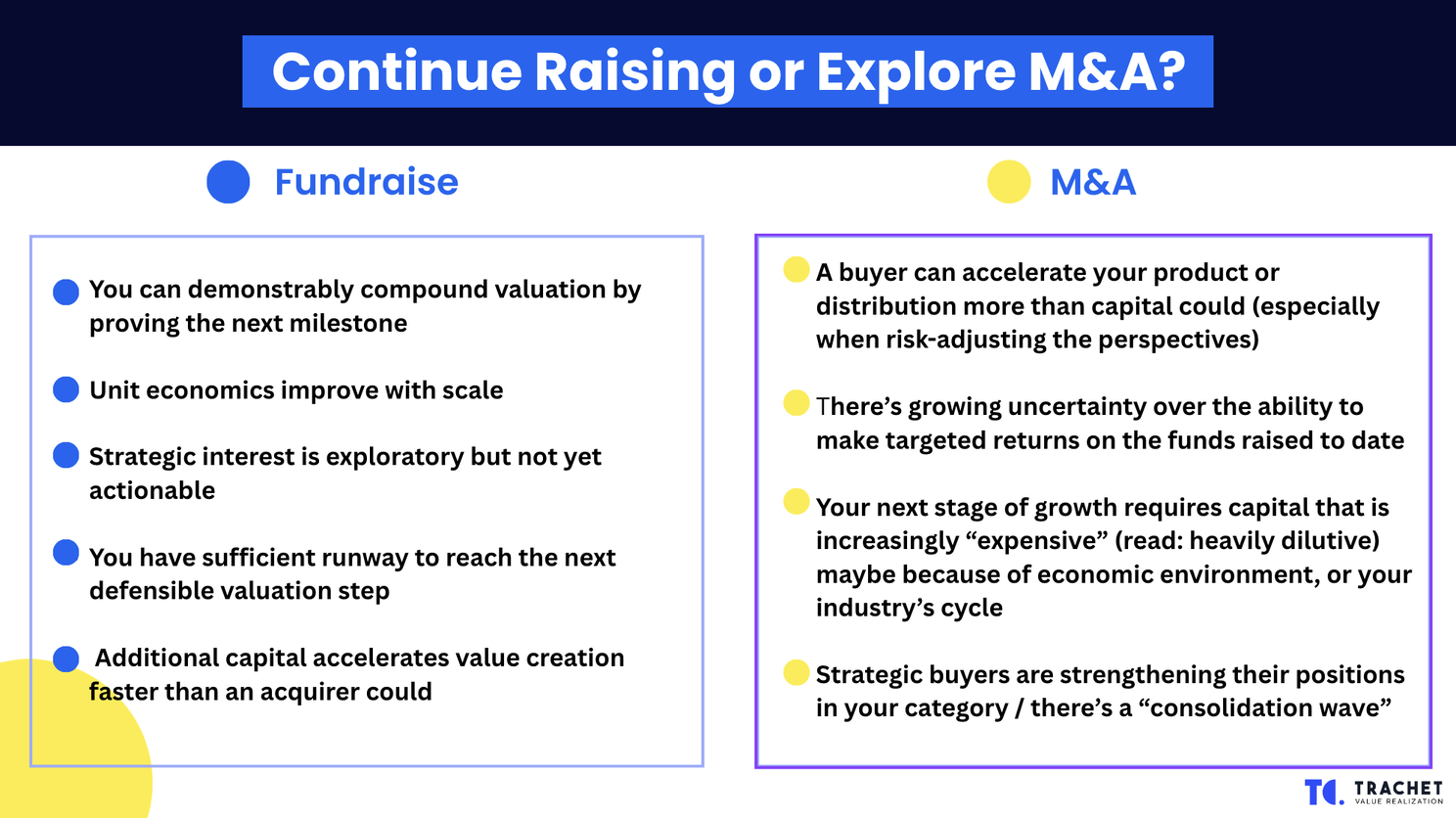

2. How Founders Decide: Continue Raising or Explore M&A?

The decision to raise or sell is rarely binary - view it as a complex decision tree. The strongest founders anchor each step towards decisions not in sentiment, but in evidence: runway, revenue quality, unit economics, buyer logic, and the efficiency of capital… and economic environment at the time + perspectives.

When continuing to raise is rational:

Put simply, continuing to raise is rational only when you can use additional capital to deliver - with reasonable confidence - more than 3x the value of that capital. That is the minimum return profile most investors target. But once a company approaches the ~$300m valuation ceiling, compounding at that level becomes structurally harder, and the balance between raising and exploring strategic options should be reassessed.

When exploring M&A is rational:

M&A becomes the right path when your product is more valuable in combination to another organisation than on its own - with no credible perspective in sight for that to change.

Read more about Dual-Track Strategy.

3. Why Timing Matters, which includes your market cycles

While most successful exits happen at specific company inflection points - because the business was positioned at the right moment in its trajectory - market cycles and overall economic environment matter as they’re defining your next “exit option” if not taking this one.

Three timing moments consistently drive strong outcomes:

1. Category consolidation: Strategics set the tempo. Moving early in a consolidation wave often produces the highest premiums. Different industries have more or less cyclical trends, and more or less consolidation. The more cyclical, the more it compounds on the timing for your own company.

2. The company proves repeatability: When a business transitions from “promising” to “predictable” - product-market fit, retention, upsell, gross margin, cohorts stabilising - acquirers gain conviction.

3. A strategic adjacency unlocks: A feature becomes a product; a product becomes a platform. The buyer’s value logic expands faster than your standalone valuation.

What’s the deal monthly news roundup

Your go-to monthly roundup of key news, deals, and emerging trends to watch in the UK/EU startup arena.

→ AI down rounds rise as questions grow over Europe’s bubble - PitchBook

Leah Hodgson reports on a widening valuation disconnect in Europe’s AI sector, where median startup valuations have surged to a record €8.8m in 2025 — more than 20% higher than last year — driven by investor competition and hype in areas like legal tech and developer tools. Yet despite these soaring prices, down rounds are rising sharply: 15% of AI deals in Q3 2025 closed at a valuation cut, even as down rounds decline across the broader VC market. The divergence points to a fragile, hype-led ecosystem where capital floods into overheated niches while fundamentals lag behind.

→ Revolut notches $75 Billion valuation in latest share sale - Bloomberg

Jennifer Surane writes that Revolut has reached a striking $75bn valuation following its latest share sale — a major leap from the $45bn mark secured last year. The round drew heavyweight backing (incl. Nvidia’s venture arm), signalling enduring investor confidence in the fintech despite wider market caution.

→ The sector with 5 quarters of deal growth and a 52% rise in funding (spoiler: it’s not AI) - Sifted

Eanna Kelly reports that cybersecurity - not AI - is the standout performer in Europe’s tech landscape, with funding up 52% year-on-year and five consecutive quarters of deal growth. The surge is being driven by an AI-powered escalation in cyberattacks, from deepfakes to automated ransomware, combined with regulatory pressure from NIS2 and the EU’s new cyber resilience rules. These forces are creating sustained demand for next-generation defence tools, giving early-stage cyber startups a rare tailwind in a cooling funding environment. Yet Europe still struggles to keep its best cyber companies local: weak exit pathways, limited European acquirers, and reliance on US buyers mean many of the continent’s successes risk migrating abroad.

→ Europe needs to deliver tech promise for more years like 2025 - Reuters

Mike Dolan highlights a rare turning point for European tech markets, with the STOXX 600 on track to outperform the S&P 500 in dollar terms - a signal of renewed global confidence in the region’s innovation engine. The real momentum lies in Europe’s deep tech sectors, from AI and biotech to defence, robotics and quantum, where analysts see potential to generate $1tn in enterprise value and create a million jobs by 2030 if capital, regulation and talent strategies align. Yet Dolan warns that this promise rests on shaky foundations: Europe still trails the US and China in R&D investment, patent production, and scaling power. For 2025’s optimism to endure, the continent will need more than a single strong year — it will need sustained delivery across the entire ecosystem.

→ 'Vibe revenue’: AI companies admit they’re worried about a bubble - CNBC

Arjun Kharpal reports growing unease among AI founders and executives who warn that valuations in the sector have become “pretty exaggerated,” with some startups effectively priced on “vibe revenue” rather than meaningful sales traction. Leaders from DeepL and Picsart argue that the mismatch between revenue realities and investor expectations is creating the conditions for a bubble - even as they remain bullish on AI’s long-term enterprise demand, particularly from 2026 onwards. Meanwhile, investment continues at an extraordinary pace, with an estimated $4tn expected to pour into data centre capacity over the next five years. The question now is whether this infrastructure boom reflects genuine future demand or marks the high-water point of AI exuberance.

→ Is Big Tech spending too much money? – Financial Times (Lex)

The FT’s Lex column questions whether Big Tech’s unprecedented investment spree in computing power, AI hardware and data-centre infrastructure is creating long-term value or fuelling a speculative bubble. Capital expenditure across the sector has surged to historic highs as companies race to dominate the next generation of AI models and cloud services. But the piece argues that without proven, scalable business models to justify this outlay, the industry risks repeating past cycles of overbuild and disappointing returns. The arms race may accelerate innovation, but unless revenue catches up with capex, today’s spending boom could look dangerously overextended.

We’re keen to hear about the key challenges (or opportunities!) shaping your company’s objectives in Q4 of 2025. Email us at claire@trachet.co for more information on topics you'd like to see discussed in future issues of What’s the deal?